KNOW YOUR RIGHTS AND DON’T GET ABUSED

If You Think Your Rights Have Been Violated, Call 877-631-6627 or email [email protected] for Your FREE Consultation TODAY. To submit an online request for a consultation, click here.

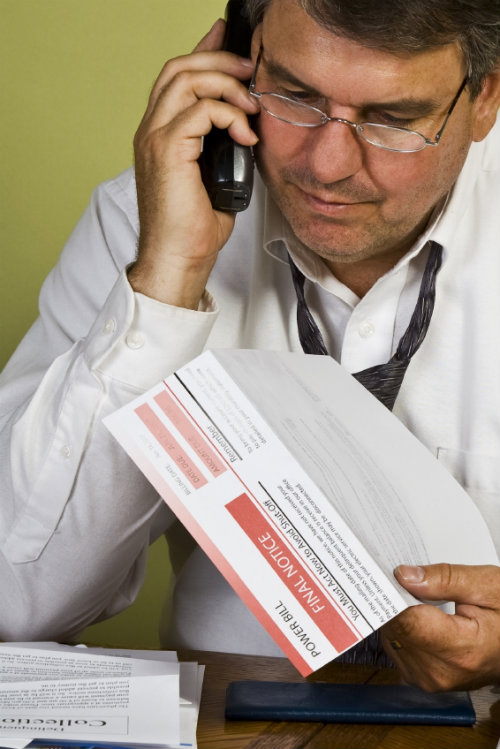

The Fair Debt Collection Practices Act (FDCPA) was enacted by Congress to eliminate abusive debt collection practices, and to provide consumers with an avenue for disputing and obtaining validation of debt information. Many debt collection agencies violate the FDCPA during their contacts with consumers, and it’s important for you to know your rights. The FDCPA provides a laundry list of what debt collectors can and cannot do in their attempts to collect a debt, as well as other things debt collectors must do when communicating with you. Hussin Law uses the FDCPA to STOP abusive debt collection.

If a debt collector violated your rights under the FDCPA, you are entitled to up to $1,000, and the debt collector pays your attorneys feels and costs. If you are getting automated calls on your cellular telephone from a debt collector or creditor, you may also be entitled to $500 PER CALL under the Telephone Consumer Protection Act.

ARE YOUR RIGHTS BEING VIOLATED?

Debt collection abuse comes in many different forms and it’s important to discuss your individual situation with an experienced consumer attorney. Debt collectors, creditors, banks, credit card companies, and collection lawyers are all prohibited from violating your rights under various applicable laws.

The following are some common illegal collection practices:

-

-

Harassment

- calling you constantly, multiple times a day for successive days in a row, back to back calls, or continuous calls after you requested the calls stop;

- repeated calls with no messages, hang-ups;

- using social media networks like Facebook to contact you;

- misleading or false comments, belittling or oppressing comments, robo-dialing, embarrassing or rude conduct;

- Many other types of conduct can qualify as illegal harassment, and you should consult with an experienced consumer attorney to analyze your individual case.

-

-

Collecting on Debts Not Owed

- No debt collector, including banks and collection agencies, are permitted to attempt to collect more than what is owed. This includes late fees if you have paid on time, penalties, a higher interest rate, attorney fees, and miscellaneous costs that are not authorized by law or contract

-

Illegal Threats

- It is illegal under the FDCPA to threaten you with arrest, or tell you that you will face criminal prosecution if you don’t pay.

- It is illegal to threaten that your wages will be garnished in most circumstances, or that your credit will be ruined.

- The collector cannot make threats to sue you unless it is both legal to take the action and the collector intends to do so.

-

Phone Calls at Work

- It is illegal for a collector to call your place of employment after you have told them not to call you at work. You do not have to put this request in writing.

- It is illegal for a collector to speak to your employer or a co-worker or leave a message regarding the debt.

-

Contacting Family Members or Third Parties

- If the debt collector knows where to reach you, they are not allowed to call any third parties.

- Unless a collector has your permission, they may not speak with anyone else about the debt. This includes family members, friends, co-workers, and employers.

- Collectors can call third parties only in an attempt to locate you. Once a collection agency knows where you are and how to reach you, calls to any third party (other than your spouse) are illegal.

-

Cease and Desist

- If you send a cease and desist letter, the debt collector may no longer contact you under any circumstances.

- If you tell a collector not to only communicate with you in writing, it is illegal to continue to call you.

- Even if you don’t send a letter, if you have told a collection agency to stop calling you multiple times, it is illegal if they ignore your request and continue to harass you with calls.

-

“Mini-Miranda”

- A debt collector must identify themselves as such when they contact you.

- A debt collector must advise you during the beginning of the call that it is an attempt to collect a debt.

-

Misrepresentations

- It is illegal to tell you that they will seize, garnish, attach, or sell your property or wages, unless they are permitted by law to take the action and intend to do so

- It is illegal to tell you that legal action will be taken against you, if doing so would be illegal or if they do not intend to take the action

- It is illegal to give false credit information about you to anyone, including to a credit reporting agency

- It is illegal to send you anything that looks like an official document from a court or government agency if it is not.

- It is illegal to lie or make false statements in their attempts to collect a debt.

- It is illegal to falsely claim to be an attorney or government representative or credit reporting agency

- It is illegal to make you think you committed a crime or that you can be arrested for not paying a debt

- It is illegal to misrepresent the amount or legal status of money you owe

- It is illegal to indicate that documents are legal forms if they are not

-

Unfair Practices

- Debt collectors may not engage in any unfair practices when they try to collect a debt from you.

- They cannot try to collect any interest, fee, or other charge on top of the amount you owe, unless the contract that created your debt–or your state law–allows the charge;

- It is illegal to depositing a post-dated check early

- It is illegal to take more money out of your account than what you authorized

- It is illegal to use your credit card or bank account information to make a withdrawal from your account unless you authorized it, even if you gave them your account information for a previous payment.

- It is illegal to take or threaten to take your property unless it can be done legally.

-

Zombie Debts

- Debt collection agencies know that zombie debts (or old, unpaid debts) are profitable. Collection companies purchase the old debts for a fraction of their value and then aggressively attempt to collect the full value from the debtors.

- Collection agencies often attempt to collect on old debts that are beyond the statute of limitations.

- If you do have an old zombie debt, you may not be legally obligated to pay it. A collector cannot threaten to report or sue you for a debt if it is beyond the applicable statute of limitations, and cannot trick you into making a small payment to revive the debt.

- If you have been contacted from a collection agency about an old debt, or a debt which you have no legal responsibility to pay, a consumer protection lawyer can help you.

-

Automated Calls

- If you are receiving unconsented automated calls on your cellular telephone from a debt collector, your case might be worth much more than $1,000.00. In fact, under certain circumstances EACH CALL is worth $500, sometimes even more.

- If you never gave your cell phone number to the creditor or if you requested that the calls stop, and you are getting automated calls on your cell phone, you could be entitled to $500 per call under the Telephone Consumer Protection Act.

- For more information on Telephone Harassment, CLICK HERE.

If Your Rights Have Been Violated, Call 877-631-6627 Today, or email [email protected] to arrange for a free consultation.

If you have been harassed by a debt collector, Hussin Law can stop the abuse and you may be entitled to up to $1,000.00. If the collection agency is autodialing your cellular telephone without your consent, you could also be entitled to $500 per call under the Telephone Consumer Protection Act. Many debt collectors will only stop violating the law when an attorney gets involved, and they are not intimidated by a consumer who does not have legal representation. Most often, collection agencies assume the consumer is unsophisticated and has very little understanding of their legal rights. Unless you get help from an attorney, the abusive conduct rarely goes punished and the aggressive collection tactics work.

Tammy Hussin has successfully settled over 1,000 FDCPA and TCPA cases, and has earned over two million dollars in settlement awards for her clients. Click Here to see that Tammy’s clients love her, and Hussin Law wants to help you, too.

If Hussin law takes on your case and cannot get a settlement, YOU OWE NOTHING. The debt collection agency pays attorney’s fees and costs in a successful settlement, and if your case does not result in a settlement, you do not pay a dime.